In the area of autonomous driving the German vehicle manufacturers BMW, Daimler and Volkswagen are pursuing individual strategies that in terms of content are very similar. For not losing opinion leadership in this technologically complex topic in favour of technology providers who were once outside the industry, a common cooperative approach is necessary. Only in this way a skilful positioning of the German automotive industry on the newly sorted mobility match field can be ensured. BMW and Daimler went first steps.

Introduction

BMW and Daimler announced details on a number of joint ventures in the context of mobility services last week. Even though autonomous driving was not yet an issue at the joint press conference, or questions were answered in an evasive manner, rumours of possible cooperation between the major German automobile manufacturers BMW, Daimler and Volkswagen, including the leading suppliers Bosch and Continental, aiming at jointly developing autonomous driving and electromobility, condensed. Today, the former rivals BMW and Daimler have finally announced that they will jointly tackle the development of a platform for autonomous driving up to automation level 3/4 in the future and bring the technology into series production by 2025. If one looks at the hustle and bustle in the field of autonomous driving in recent years, this is a long overdue drumbeat of the German automotive industry, that hitherto is certainly bustling but nonetheless seems to be a bit lethargic when compared to US and Chinese players.

Mobility providers have built up a profitable business in recent years based on the ever-changing social mobility needs, which they are now partially completing in a consistent second evolutionary step with self-driving vehicles. These include, for example, the US Ride-Hailing providers Lyft and Uber or the French chauffeur Privé. And recently, the above-mentioned Jurbey by BMW and Daimler is blessed with the best conditions at this point.

Technology providers, in contrast, focus on different specific, primarily technological challenges of autonomous driving. Powerful on-board computers for the evaluation of multi-sensor systems (Sensor Fusion ECU) in real time and for the realization of machine learning methods (e.g. Intel, Nvidia), camera-based systems and image recognition methods (e.g. Mobileye) or lidar-based systems (e.g. Luminar) are examples. In addition, the Google sister Waymo, the GM subsidiary Cruise Automation or the US startup Aurora provide holistic solutions including the necessary sensors and vehicle integration.

Automotive suppliers such as Bosch, Continental or ZF are increasingly involved in these developments. Bosch already being the leading AI provider in the automotive industry, has recently set itself the AI world-class target by 2021 and thus is investing vigorously. Delphi has also repositioned itself on the new core business of networking and autonomous driving by splitting off the powertrain business and renaming to Aptiv.

Increasingly, the boundaries of this classification are blurring, and suppliers are positioning themselves within the forming business areas. AI technologies are becoming increasingly relevant to automobile manufacturers (OEMs), so that traditional automotive suppliers specialize into AI technology providers and open up the field of mobility providers in cooperation with OEMs. In contrast, the leading technology providers exploit their technological edge and directly become the top dog automotive suppliers for AI systems in the field of autonomous driving.

Autonomous Driving – A joint effort

Given the complexity of the topic and the required expertise in the innovative hardware and software technologies involved, supplementary collaborations between the players are not surprising. In particular, the OEMs are still dependent on specialized cooperation. Different strategies can be observed among the German OEMs, also based on their different levels of experience.

Volkswagen AG

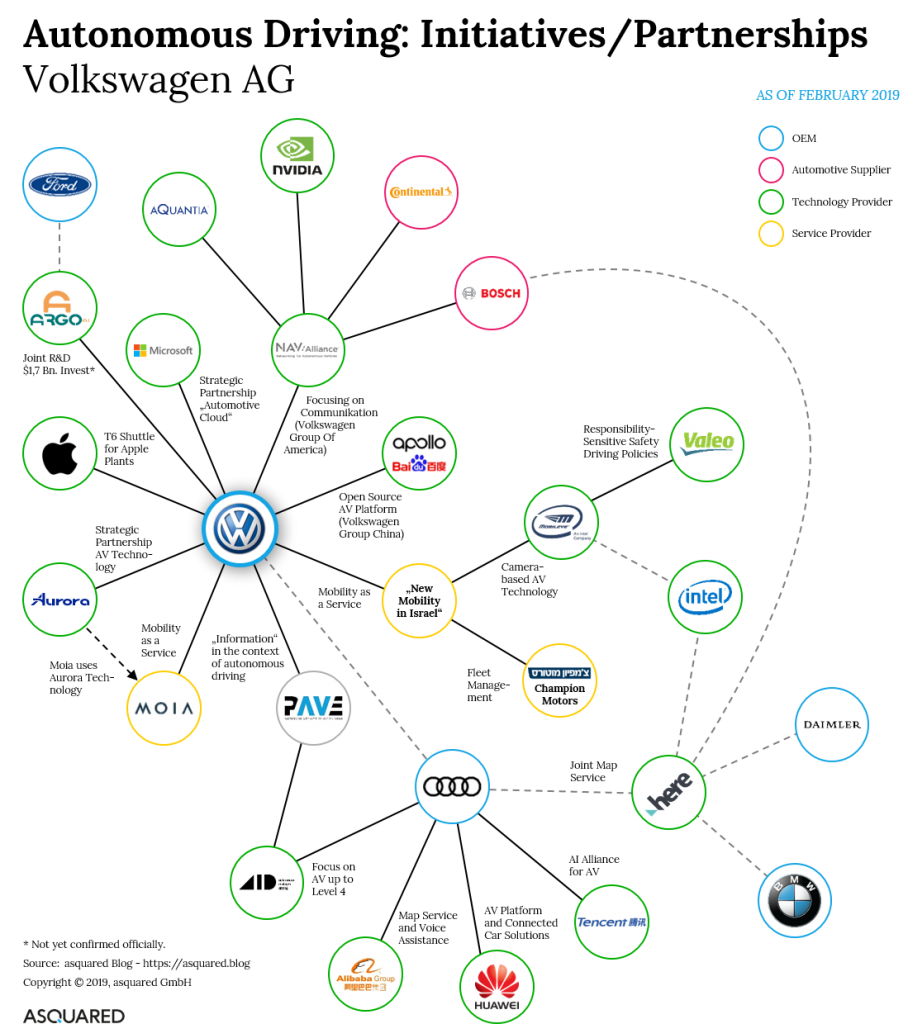

In the field of autonomous driving, Volkswagen has positioned itself broadly and apparently pursues a multi-pronged strategy, thus trying to be on the safe side.

On the one hand, Volkswagen is developing a ride-hailing service with autonomous and electric vehicles in Israel as part of the “New Mobility in Israel” initiative. Development is scheduled for 2019 and availability in 2022. Technologically, the mainly camera-based systems of the Intel subsidiary Mobileye will be used, as well as Valeo‘s Responsibility-Sensitive Safety Driving Policies, a set of regulations for good and safe driving to be followed by the vehicle.

On the other hand, Volkswagen is cooperating with Aurora, a provider of a complete platform for autonomous driving, which also relies on lidar sensors. Aurora is still a relatively young company, led by industry leaders of the pioneers of autonomous driving Alphabet, Tesla and Uber. Volkswagen seems to trust this trio and the concept a lot. According to rumours, Volkswagen was aiming for a takeover last year, which has been rejected by Aurora. The Volkswagen mobility service Moia uses Aurora technology. Piloting of the service is scheduled for April 2019 in Hamburg.

“We must acquire the technologies for this in China or on the US West Coast, unless we have the capacities ourselves.”

Dr. Herbert Diess, CEO of Volkswagen AG

These level 4/5 approaches are undertaken by Volkswagen itself as part of the outlined cooperations. In-house developed solutions up to level 3/4, on the other hand, are driven primarily by the premium brand Audi and the Audi subsidiary Autonomous Intelligent Driving (AID), which was spun off in the spring of 2017. By 2021, self-driving vehicles shall be brought to the streets. Audi also has cooperation agreements with Chinese players, such as Alibaba, Huawai and Tencent, as well as participation in its own cross-OEM mapping service Here.

Volkswagen also has a strategic partnership with Microsoft to establish the “Volkswagen Automotive Cloud” and Apple to provide T6 vans for Apple’s self-driving factory shuttles and is also a member of China’s leading autonomous driving technology consortium, the Baidu platform Apollo. Within the NAV Alliance (Networking for Autonomous Vehicles) standards for the high technical challenges in the area of communication within the vehicle are being developed in cooperation with the suppliers Bosch and Continental.Recently it was reported that Volkswagen plans to invest with 1.7 billion USD in the Ford subsidiary Argo AI and rise to an equivalent investor next to Ford. The research in the field of autonomous driving would be done in cooperation with Ford. To what extent these activities are synchronized with the work of the Audi subsidiary AID is not clear.

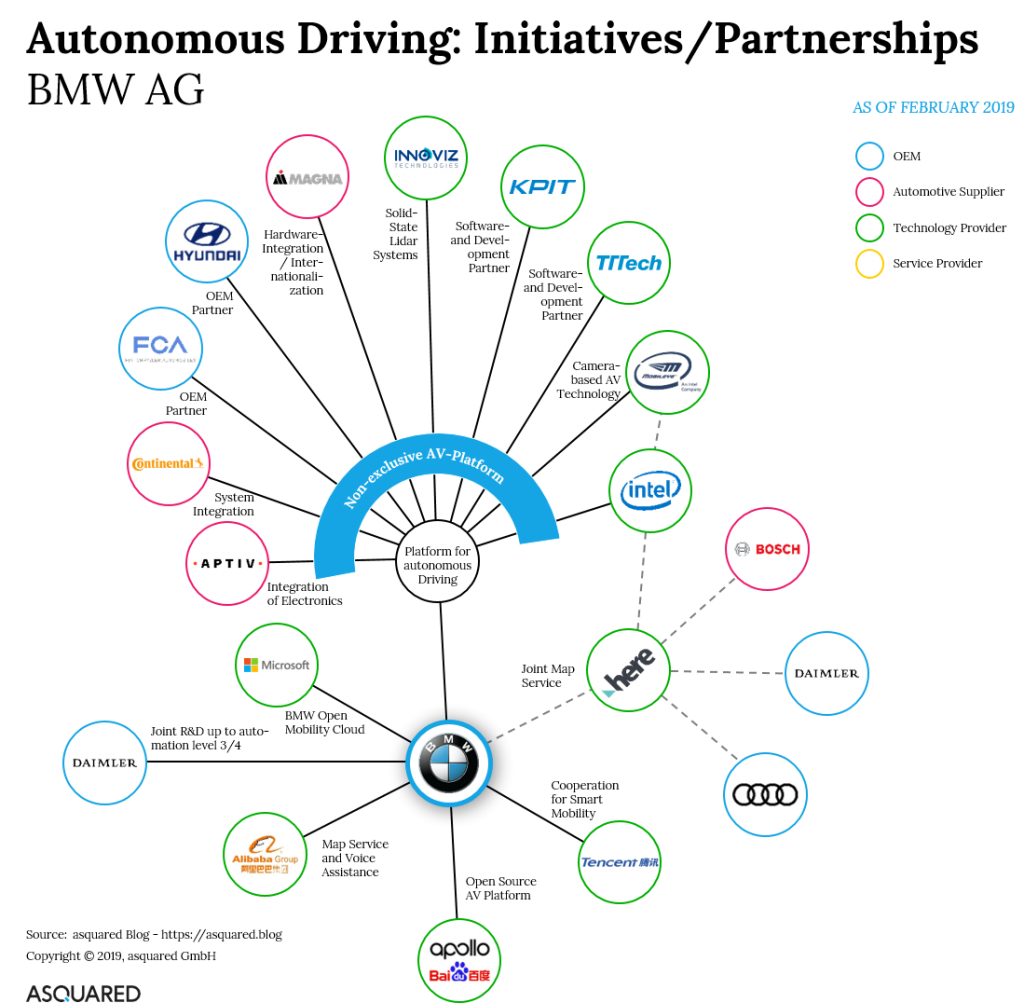

BMW Group

Compared to Volkswagen, the BMW Group seems to be much more focused and, in the area of autonomous driving, obviously focuses on self-development.

“We are at war of technology.”

Harald Krüger, CEO BMW AG

For example, BMW is the patron of an industry-wide alliance that has set itself the goal of developing a non-exclusive and flexible platform for autonomous driving with the functions “Highway Pilot” and “Urban Pilot”, and building on this, of bringing vehicles with automation level 4 / 5 to mass production in 2021. At BMW it is about the iNext.

Various suppliers such as Aptiv, Continental and Magna, as well as the OEMs Fiat Chrysler Automobiles and Hyundai are involved in the partnership. Aptiv assumes the role of technical integrator for electronic components, while Continental assumes the role of system integrator and supports the topics of motion control, simulation and validation. Magna supports hardware integration and aims to make the technical platform globally available. Technologically, the software development partners KPIT and TTTech are on board and for the basic image recognition, AI and computing technology Intel and Mobileye are used. BMW also relies on Solid-State Lidar systems from Innoviz.

Today it was announced that BMW and its competitor Daimler are also working together to develop a platform for autonomous driving after they already established a cooperation in the area of mobility services. The focus would be on automation level 4 and on the way to mass production in 2025, the functions of driving on the highway and automated parking functions will be implemented. The forces are pooled to exploit synergies in development costs and drastically reduce development times.

BMW is also heavily involved in China. For example, BMW has joined the Baidu platform Apollo as a board member and is cooperating with Alibaba and Tencent on integrating the service platforms into the vehicles. BMW was the first international vehicle manufacturer to receive a license to test its self-driving vehicles in Shanghai in certain areas of public roads.

Like Volkswagen, BMW relies on the Microsoft Azure cloud for online and connected services, the “BMW Open Mobility Cloud”; Card services are addressed through the Joint Venture Here.

Daimler AG

Daimler seems to be focused similarly, but with a much higher degree of exclusiveness. Daimler has been involved in research on autonomous driving for many years. In the field of research, Daimler was already one of the first cooperation partners of Apple and Google, when they began dealing with the subject of mobility more than 10 years ago.

“We will have completely new competitors.”

Dr. Dieter Zetsche, CEO of Daimler AG

Daimler is currently working closely with the supplier Bosch on the development of vehicles with automation level 4/5, relying on the Nvidia Drive Pegasus AI platform. The partnership intends to test its self-driving vehicles (Mercedes S- and V-Class) in the second half of 2019 in California as part of a shuttle service.

Daimler was one of the first cooperation partners of the Baidu platform Apollo in 2017 and also cooperates with Baidu and Alibaba on the integration of their service platforms and mobility services. Daimler was the first international vehicle manufacturer to receive the necessary license from the Chinese capital Beijing to test self-driving vehicles last year. Since today, the cooperation with BMW on autonomous driving is official.

Are these approaches enough?

Autonomous driving goes well beyond self-driving vehicles. In order for autonomous driving to actually become safer than human driving, in addition to the perceptual and conclusive abilities of the vehicles – which it undoubtedly needs – further relevant framework conditions have to be created and technological hurdles have to be overcome. Safe autonomous driving requires the existence of at least the following components.

- Self-driving vehicles, which have a macro view (reliable maps) and a micro view (sensors, such as camera, radar, lidar, sonar) of their current environment and can evaluate them in real time and draw conclusions on this basis. The software component between the sensor and the actuator is the crux of the matter here.

The majority of players focus on the technological development of self-driving vehicles, as it is very promising with a short-term perspective. The technologies are mature and tested and are already in the optimization phase. By contrast, the topics listed below are (in any case publicly known) addressed only occasionally. - Comprehensive data base – The quality of the data base as well as the amount of data is decisive for the probability of success of the machine learning methods used. The inter-vehicle and multi-vendor communication of data to improve the data foundation for the AI components (training data and model data) enables collaborative learning. The resulting database represents the essential asset.

- Car2X communication – An efficient exchange of data between vehicles (Car2Car) and between vehicles and their surrounding infrastructure (Car2Infrastructure) provides a significant additional information channel for autonomous vehicles. For example, information about intended driving manoeuvres, observed dangerous situations or information from traffic management systems can already be transmitted in advance and synchronously to the road users in the immediate vicinity.

- Modern IT Infrastructure – The basis for autonomous driving is essentially the software, which is why speed is decisive in the development process. For example, there is an increasing need to be able to develop and roll out updates at short notice; A postponement until the next upcoming vehicle inspection is not very contemporary just as the friendly written invitation to a unscheduled visit at the contract workshop. The software must be considered decoupled from its infrastructure – the vehicle. This requires modern development and deployment paradigms. Technically, over-the-air updates have long been possible. Unfortunately, most OEMs need massive restructuring of the internal organization, a modernization of the technical infrastructure and a fundamental overhaul of the distribution structures.

- Legal framework – Autonomous driving would like to be well regulated throughout the EU. The technology is being promoted in the USA and China, and the legal frameworks have long been in place. Admittedly, the legal situation in the EU with the state authorities and the EU and UN bodies is complex and specific. Nevertheless, the EU currently falls behind again and should revalue their position by granting permits in selected European cities as fast as possible.

Autonomous driving is thus a strong technology- and software-focused discipline with far-reaching interactions in key areas of all parties involved. All the points mentioned have something in common: they naturally require the coordination and cooperation of several parties and they are necessary activities, that are not going to differentiate the competition in the near future. Close cooperation, especially at OEM level makes perfect sense. BMW and Daimler are thus taking a meaningful and necessary step in the absolutely right direction.

Cooperations as a prerequisite for autonomous driving

The German automotive industry has long been at the forefront of vehicle hardware, from powertrain and engine technology, safety technology, to body construction with excellent gap dimensions. With the advent of electromobility and the increasing relevance of software-based systems in and around the automobile, these former success factors are increasingly losing relevance in differentiation from the competition, or are becoming completely obsolete. The hardware becomes the infrastructure. The focus is now rather on the user interface to the vehicle, intuitive interfaces, maximum integration and interaction across all channels, or even just mobility as such. Software competence is becoming an essential distinguishing feature and is currently found in the area of autonomous driving in orders of magnitude outside Germany or even Europe.

With regard to the German OEMs, it can be observed that great efforts are being made to develop self-driving, networked and smart vehicles – with a more or less pronounced focus on organically building up the required expertise. The three German OEMs under consideration (BMW and Daimler itself, Volkswagen via Audi) are currently working in parallel and, with the exception of the recently announced collaboration between BMW and Daimler, competing with each other for the same technological challenges and cooperating partly with the same technology providers. The AI know-how, which is essential for autonomous driving, is built up in separate silos together with the OEM, while technology providers such as Waymo and Aurora achieve significantly more extensive and differentiated data collection in partnerships with several OEMs – this is reflected in the reliability and quality of the AI systems.

“Once being a car country, germany is threatened to becoma a supplier nation.”

Christoph Bornschein, TLGG

The German and European vehicle manufacturers should remain at the wheel when it comes to opinion and technology leadership in the field of autonomous driving. Compared to Baidu and Waymo, for example, this race seems long lost. At the same time, not all problems have been solved: the streets of California’s metropolises, where Waymo vehicles predominantly operate, are nowhere near the complexity of European road networks; their usage far-off grid-shaped road planning still must be proven. The database is maintained defensively for each technology provider in competition to everybody else; there are no established participation models, the full potential of the technology is not tapped. Cross-vehicle communication paradigms are not yet widely available and not yet sufficiently integrated in the context of autonomous driving.

From a European or even German perspective, an OEM-wide cooperation to develop a complete platform for autonomous driving is indispensable. Such a platform technology- inherently can be successful only on a large scale. One OEM alone will never achieve the required market coverage due to the competition with the other OEMs. By contrast, cooperations with technology providers cannibalize their own significance in the long term. As was already the case with the airbag, the ABS and other driver assistance systems, these innovations can only be used as a competitive advantage by the innovation leader in the short term. In the medium to long term, they become a standard, as a matter of course. The same will be the case for autonomous driving along its five levels of autonomy.

The consideration must go beyond competition about the vehicle buyer between the OEMs in terms of the pure functionality and time; The viewing angle has to be widened considerably. Rather, the topic has the potential to decisively influence the future positioning of all participating players in the changing field of mobility. And it is open if these players are individually able to decide this game for themselves. The cooperation between BMW and Daimler is therefore the first step on the required common path of the German or even European automotive industry.

Will our future self-driving vehicles be controlled by non-European search engine vendors, or is the European automotive industry able to position itself as a global technology provider of a holistic autonomous driving platform, tapping into innovative business models – from the obvious mobility service provider for waterborne, rural and air transportation to a purely data-driven service provider?

I would prefer the latter.

References

- Automobil Industrie, “Magna beteiligt sich an Plattform für autonomes Fahren”, 12.10.2017, Link

- Automobil Produktion, “5GAA, BMW und andere zeigen C-V2X-Technologie”, 17.07.2018, Link

- Automotive News Europe, “In self-driving car race, Waymo leads traditional automakers”, 08.05.2018, Link

- Automotive News, “Intel and Mobileye forge new partnerships with Volkswagen and Valeo at CES”, 10.01.2019, Link

- Autonomes Fahren & Co, “BMW & Mercedes-Benz gehen zusammen?”, 21.01.2019, Link

- Autonomes Fahren & Co, “Deutsche Autoindustrie vereint beim Autonomen Fahren?”, 24.01.2019, Link

- Autonomes Fahren & Co, “Jurbey und Urgent.ly”, 25.01.2019, Link

- Autonomes Fahren & Co, “VW investiert bei Argo AI von Ford”, 27.02.2019, Link

- BMW Blog, “BMW and Daimler Announce Agreement for Autonomous Driving R&D”, 28.02.2019, Link

- BMW Blog, “BMW shares with us its autonomous technology roadmap”, 29.10.2017, Link

- BusinessWire, “Volkswagen, Mobileye and Champion Motors to Invest in Israel and Deploy First Autonomous EV Ride-Hailing Service”, 29.10.2018, Link

- China Daily, “Audi gets license to test autonomous vehicles in China”, 17.09.2018, Link

- Continental, “Continental Joins Autonomous Driving Platform from BMW Group, Intel and Mobileye as System Integrator”, 20.06.2017, Link

- Daimler, “Daimler erhält als erster internationaler Autobauer Genehmigung für Erprobung von vollautomatisierten Fahrzeugen auf öffentlichen Straßen in Peking”, 06.07.2018, Link

- Daimler, “Mit BMW zum nächsten Level beim automatisierten Fahren”, 28.02.2019, Link

- Elektronik automotive, “BMW holt KPIT und TTTech als Partner an Bord”, 24.10.2018, Link

- Handelsblatt, “„Noch ist es nicht zu spät“ – VW-Chef Diess warnt vor Abhängigkeit in der Batteriezellentechnik”, 21.08.2018, Link

- Handelsblatt, “Alibaba deal with Daimler, Audi, Volvo shows China role in industry future”, 23.04.2018, Link

- Handelsblatt, “Milliarden fürs autonome Fahren – Bosch wagt sich ins KI-Duell mit Google”, 30.01.2019, Link

- Handelsblatt, “VW, BMW and Daimler hold talks on cooperation in self-driving cars”, 25.01.2019, Link

- Handelsblatt, Christoph Bornschein, “Deutschland droht vom Autoland zur Zulieferernation zu werden”, 30.01.2019, Link

- Internet of Business, “Apple partners with Volkswagen on driverless vehicles”, 24.05.2018, Link

- Internet of Business, “Data highway: Autonomous vehicles and the connectivity challenge”, 29.01.2019, Link

- Microsoft News, “Volkswagen und Microsoft gehen strategische Partnerschaft ein”, 28.09.2018, Link

- NGIN Mobility, “Wie die europäische Politik das autonome Fahren ausbremst”, 16.07.2018, Link

- Pandaily, “Tencent & BMW Signed Strategic MoU to Promote Integration of Digital Platforms”, 06.09.2018, Link

- Reuters, “VW taps Baidu’s Apollo platform to develop self-driving cars in China”, 2.11.2018, Link

- SlashGear, “Daimler and Bosch autonomous car ride-hailing starts 2019”, 08.11.2018, Link

- Süddeutsche Zeitung, “Wie VW seinen Rückstand beim autonomen Fahren aufholen will”, 21.01.2019, Link

- TechCrunch, “Audi, Mobileye, Waymo, other top automakers unite to spread the self-driving gospel”, 07.01.2019, Link

- TechCrunch, “BMW is working with LiDAR company Innoviz to make self-driving cars”, 26.04.2018, Link

- The Drive, “Daimler-BMW Mobility Services Joint Venture To Be Named “Jurbey””, 22.01.2019, Link

- The Drum, “Tencent forms alliance to develop artificial intelligence in self-driving vehicles”, 28.08.2017, Link

- The Verge, “Audi pulls the curtain back on its self-driving car program”, 18.12.2018, Link

- The Verge, “Audi taps Huawei to help power self-driving cars in China”, 12.10.2018, Link

- VentureBeat, “Bosch and Daimler partner with Nvidia for self-driving car platform, plan to start testing in 2019”, 10.07.2018, Link

- Vision Mobility, “BMW darf als erster internationaler Autohersteller in Shanghai autonom testen”, 17.05.2018, Link

- Volkswagen, “Volkswagen steigt bei Baidu-Plattform Apollo ein”, 02.11.2018, Link